Welcome to this week’s Property News.

The week was much quieter in terms of transactions than previous weeks with just $900m in sales with a few major deals by Charter Hall totalling $343m absorbing the headlines.

The Group’s acquisitions included the historic Treasury Building at 130 William Street Brisbane for $248m and the acquisition of industrial sites in Minto for $75.3m and Brendale for $19.7m.

With the Minto asset trading at a 3.3% yield, the market is beginning to wonder whether industrial assets are being accurately priced, after all they are generally characterised by a single tenant exposure with a higher likelihood of building obsolescence. The danger here is in making generalisations from several real estate deals, as each trade is priced individually and subject to a range of current and local issues and opportunities.

Large scale industrial land is currently experiencing short supply conditions and rising demand and whilst there are large areas of future industrial land to be developed, much of this is tied up in planning and servicing constraints. This will naturally lift rents and values.

Nevertheless, the markets are concerned about the prospects of rising inflation and the potential for interest rates to move higher.

This week, the ABS released the September Quarter inflation data showing that prices increased by 0.8%, taking the annual rate of increase to 3.0%.

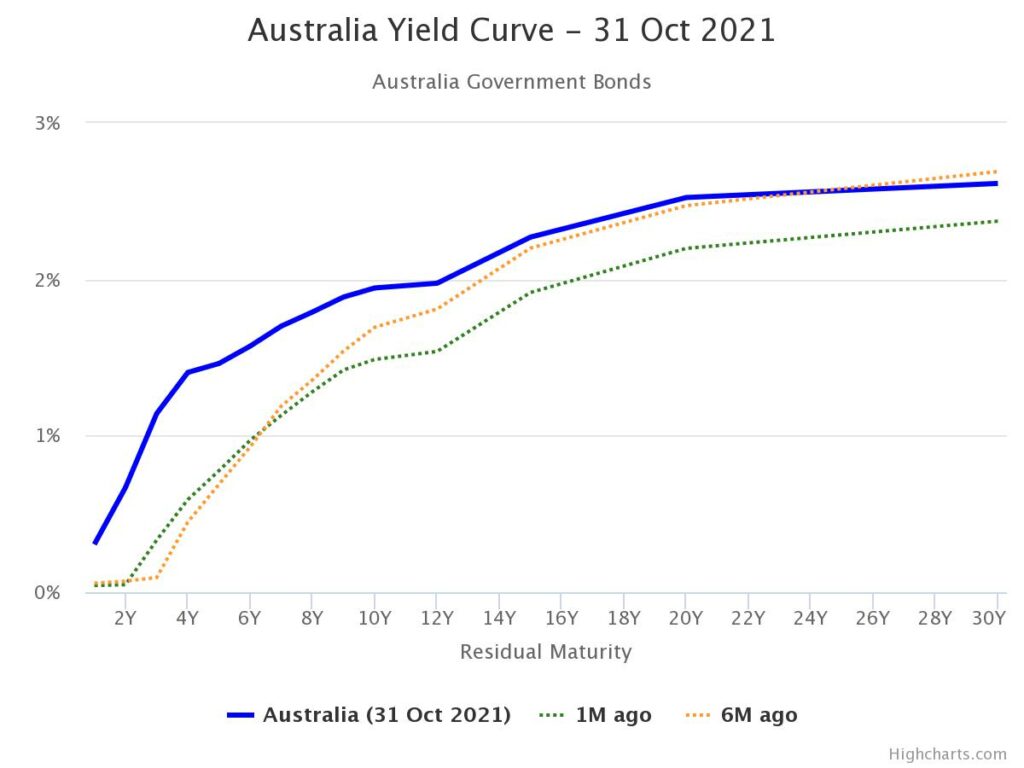

Underlying inflation, which removes impact of irregular or temporary price changes in the CPI (such as the significant fuel price increases this quarter or the impact of free childcare in 2020), recorded the strongest annual increases since 2015. The trimmed mean inflation increased to 2.1 per cent, up from 1.6 per cent in the June quarter.

Whilst these rates are within the RBA target range for inflation, the markets are expecting the Reserve to have to bring forward interest rate hikes to keep inflation under control. These expectations are reflected in the bond yields which have risen considerably over the past month. Ten year bonds are currently 60bps higher than 1 month ago.

Pricing real estate in an environment of increasing inflation is challenging and some groups will get this wrong. Rental growth assumptions, terminal cap rates, interest rates and hedging strategies all near to be examined and tested for a range of outcomes.

In these circumstances, we continue to favour investment or development property underpinned by long term secure tenants who rely on non discretionary consumer expenditure. These include neighbourhood convenience retail, medical & health facilities, education and child care services, fuel & automotive services.

The ability to capture increased income that comes with economic growth and inflation or the reversionary value that is associated with these are important. Assets with access to market rents in 4-5 years time are likely to be more valuable than those with much longer term leases.

As you would expect, we are still cautious on CBD office, hotels, regional and major / regional shopping centres but expect there will continue to be opportunistic buying that can deliver good yields.

If you have any news, information or research reports you’d like us to share with the market, please feel free to send me an email at info@propertymarkets.news or simply submit an article for us to review here.

Related Articles