A sharp slowdown in Australia’s industrial development pipeline is expected to underpin stronger absorption and renewed rental growth across key east coast markets, according to Knight Frank’s latest research.

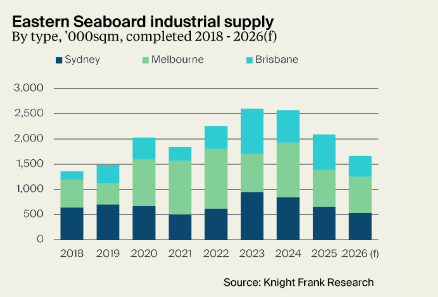

The firm’s Australian Industrial Review Q1 2026 found while east coast vacancy edged 0.1% higher to 3.9% in the first quarter of this year, new industrial supply is rapidly contracting, with 2026 completions forecast to fall a further 20%, following a 19% decline in 2025.

Total new supply across the east coast fell to 2.1 million square metres in 2025, and in 2026 there is 1.66 million square metres of new supply forecast.

The diminishing speculative construction pipeline has meant speculative space now accounts for 30% of vacancy, which is well down on 2023 levels, when development activity peaked. Speculative completions are forecast to total just around 700,000 square metres in 2026 compared to more than 1 million square metres in 2025. Pre-committed development is expected to account for almost half of all new supply, reflecting more cautious developer behaviour.

Knight Frank Partner, Partner, Research & Consulting, QLD Jennelle Wilson said the market was transitioning from a supply-driven phase to one increasingly supported by constrained development activity.

“The industrial sector is undergoing a structural reset,” she said.

“Vacancy has risen modestly, but the development pipeline has adjusted very quickly, with fewer pre-committed projects reaching fruition in 2025.

“The level of speculative vacancy is expected to be absorbed relatively quickly as the forecast pipeline slows, which will support future rental growth.”

Knight Frank’s Australian Industrial Review Q1 2026 found Sydney has the lowest industrial vacancy at 2.9%, followed by Melbourne and Brisbane at 4.5%. Within each city there is also high divergence between precincts with those exposed to substantial recent new construction seeing the highest vacancy.

Tenant activity has eased but solid underlying fundamentals remain

Despite softer leasing conditions in early 2026, fundamentals remain resilient. East coast take-up totalled 602,000sq m in Q1 this year, which was 21% lower than the five-year quarterly average, but it followed a strong finish to 2025 which saw take up reach 3.16 million square metres over the year.

“While geopolitical uncertainty poses risks in 2026, the industrial and logistics sector continues to be supported by solid underlying fundamentals,” said Knight Frank Partner, Head of Capital Markets Australia Michael Kwok.

“Structural drivers, including e-commerce growth, supply chain reconfiguration and infrastructure investment will support occupier demand, while ongoing supply constraints are expected to underpin rental growth and occupancy levels.”

The Knight Frank research found Brisbane continues to outperform on rental growth, recording the strongest annual prime effective rent growth of the east coast cities at 9.2 per cent, supported by strong face rental growth and a thinning development pipeline.

“In Brisbane, incentives appear to have peaked and in some precincts are already falling, which is helping translate face rent growth into real income gains for landlords,” Mr Kwok said.

Related Articles