Budget Changes to Redirect Private Capital Into Commercial Property: Knight Frank

25 June 2026

Proposed capital gains tax (CGT) changes in the 2026–27 Federal Budget are set to significantly reshape investment flows between different property markets, diverting private capital away from residential housing and into commercial real estate, according to new Knight Frank research.

The analysis entitled ‘Budget 2026-27: CGT change to divert private capital to CRE’, shows that the shift to inflation indexation for capital gains – alongside changes to negative gearing – will materially improve the relative attractiveness of commercial property, particularly for private investors traditionally focused on residential assets.

The new tax regime will typically see commercial property investors pay less CGT

Under the proposed system, commercial property investors would likely pay less tax than under the current 50% CGT discount, reflecting the sector’s lower capital growth profile and stronger income characteristics, while the opposite is true for residential property.

The research indicates that assets delivering capital growth below around 4.5% per annum – such as commercial property – are likely to face a lower effective tax rate under the new system, assuming inflation of 2.5% per annum – the midpoint of the Reserve Bank of Australia’s target.

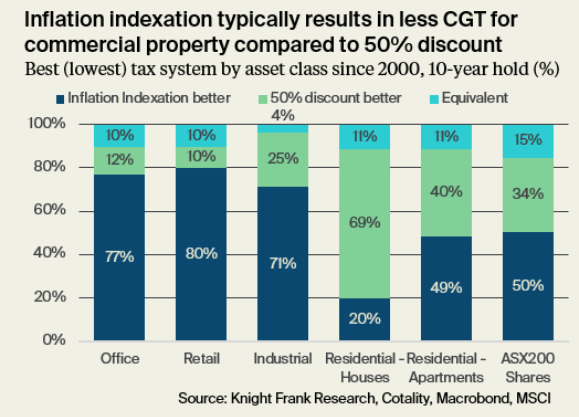

Knight Frank’s analysis of historic investment returns over the past 30 years shows that private investors in office markets would have benefited from an inflation-indexed CGT regime 77% of the time since 2000, assuming a 10-year hold period, highlighting the scale of the potential shift in after-tax returns. Investors in retail assets would have been better off 80% of the time, while investors in industrial assets would have been better off 71% of the time.

This contrasts with established homes, where after-tax returns have mostly been stronger under the existing 50% discount. For houses, capital returns have been treated more favourably under the existing regime 69% of the time, while the indexation regime would have been better only 20% of the time.

Income-focused assets win under the new system

Knight Frank Chief Economist Ben Burston said the tax changes were broadly expected to attract more private capital to commercial property, and could represent a structural turning point for investment allocation across asset classes.

“These reforms are likely to meaningfully tilt the playing field in favour of commercial property,” he said.

“Commercial assets tend to deliver the majority of returns through income rather than capital growth, so they are better aligned with an inflation-indexed CGT regime,” he said.

“The new method for calculating CGT liability favours income-driven investment over other investments offering lower income but the potential for higher capital growth.”

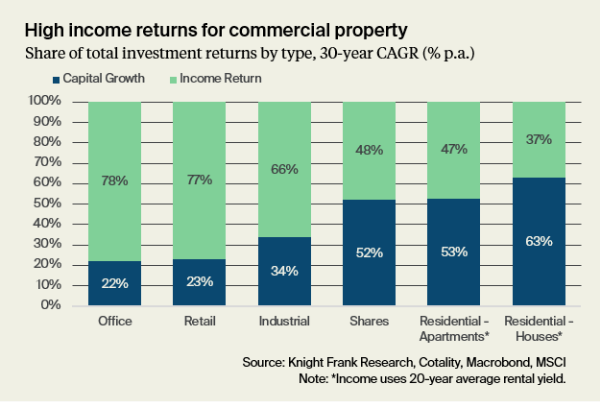

Knight Frank’s analysis found total investment returns across all major asset classes has been relatively similar over the past 30 years, averaging 8% to 10%, but what matters under the proposed tax changes is not how much return each asset has generated, but where that return came from.

Commercial real estate is typically viewed by investors as a more income-focused asset, with yields averaging around 5.5% over the past decade, while capital growth has historically been a smaller part of the investment thesis. Across the three traditional commercial property sectors, around 70% to 80% total returns have typically been derived from income.

Investors in established homes tend to have a different approach, typically buying houses on lower yields of 3% to 4% in most capital cities, and focusing on the potential for growth in property values, which has historically done most of the heavy lifting for investment returns. In residential houses and units, around 60% to 70% of total returns have been derived from capital growth

“Although total returns have been similar across asset classes, this difference in return composition translates into a material difference in after-tax outcomes under the policy,” said Mr Burston.

“Under the 50% discount, the composition of returns didn’t matter as much for tax purposes as the effective tax rate on capital gains remained the same regardless of the capital growth rate.

“But under inflation indexation, return composition matters. Indexation taxes only real capital gains — growth in value above inflation. For commercial property, where capital growth has historically run at or only modestly above inflation over the long run, the real gain subject to tax is small — lowering the CGT liability and the effective tax rate on capital gains.

“For residential investors, whose returns have largely been built on capital growth well above the inflation rate, the shift is more consequential. The real gain has tended to be much larger, increasing the CGT liability and the effective tax rate on capital gains.”

Private capital set to pivot

The proposed removal of negative gearing for established residential property purchases, combined with the retention of negative gearing for commercial property, is expected to further accelerate the reallocation of capital.

Knight Frank anticipates growing demand for standalone and smaller-scale commercial investments, including strata office, industrial units, medical centres and service stations, as private investors seek alternatives to residential property.

At the same time, new entrants to the sector are also likely to consider indirect vehicles such as REITs, unlisted property trusts and syndicates to overcome barriers to entry, including higher capital requirements and operational complexity.

Knight Frank Partner, Head of Private Office Australia Ari Petrovs said the changes would likely broaden the appeal of non-residential real estate among private investors.

“Whatever their views on the Budget, investors will need to respond to the changes and reassess their current property strategy as a result,” he said.

“One potential consequence is greater allocation to non-residential asset classes, given that the new system is well aligned to these sectors and their inherent return characteristics. The combination of tax advantages, higher income yields and the ability to retain negative gearing will make non-residential assets far more compelling, on a relative basis.

“As investors process the consequences of these changes, it’s conceivable that enquiry from privates who have historically been concentrated in residential property will start to pivot. There are of course sensible caveats to this theory, none more so than the current relative ease for private investors to get exposure to the residential investment sector across a broad spectrum of price points.

“Many high-net-worth families were already reviewing their portfolios in light of changing market conditions, but now they are hurriedly reviewing not only their portfolios, but also how they are held and structured. Don’t underestimate how this legislation is challenging the well-considered and often complex wealth management planning of many individuals and their families.”

Broader market implications

The Budget measures are also expected to prompt changes in investor behaviour beyond asset allocation.

The introduction of CGT on pre-1985 assets may drive portfolio repositioning among long-term holders, while changes to trust taxation could influence ownership structures across commercial property portfolios.

In addition, a review of superannuation fund performance tests may support increased investment into housing and alternative sectors such as build-to-rent, further reshaping capital flows across the property market.

Mr Burston said that while the reforms are still subject to parliamentary approval, the direction of policy is clear.

“If implemented, these changes will have far-reaching implications for investment strategy, encouraging a reweighting toward income-producing assets and reinforcing the role of commercial property in diversified portfolios,” he said.

Related Articles