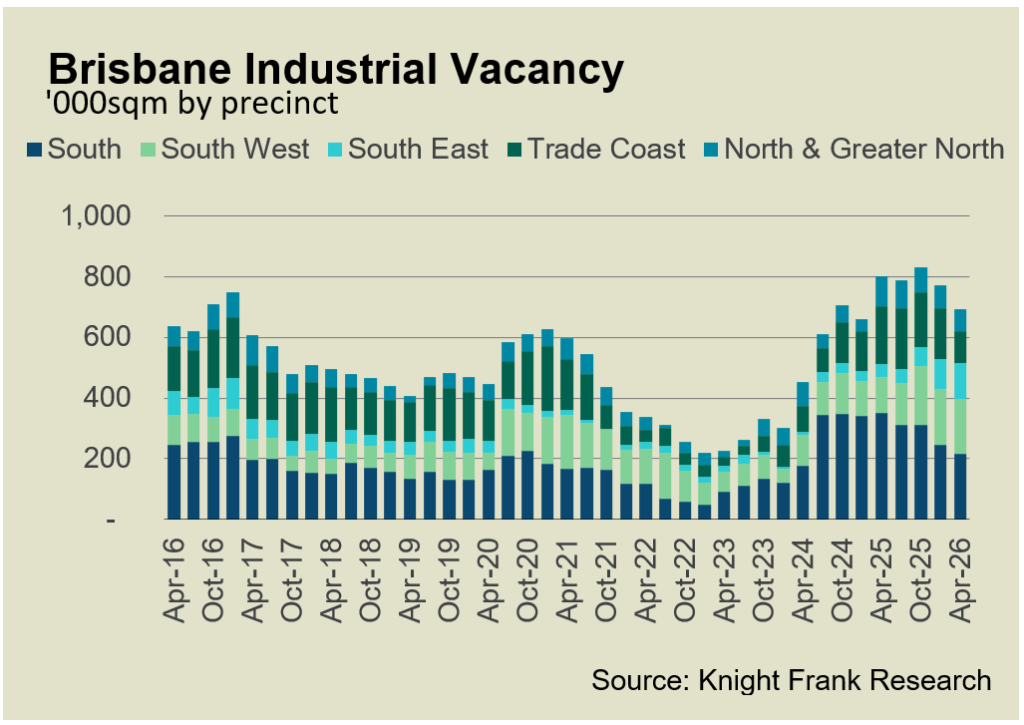

Vacancy in Brisbane’s industrial market continued to fall in Q1, and lower supply is expected to support further vacancy contraction this year, according to Knight Frank research.

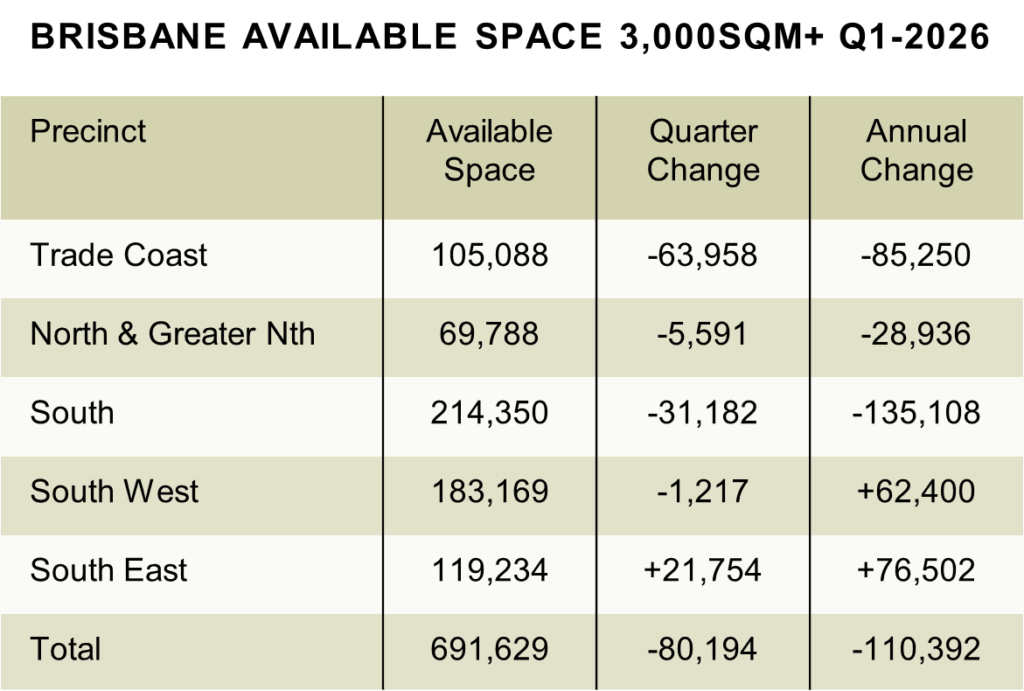

The firm’s Brisbane Industrial Precinct Update – Q1 2026 shows overall vacancy has fallen to 4.5%, from 5.4% a year earlier – a reduction of 110,392sq m – due largely to take up of speculatively developed space.

Prime stock represents 58% of current vacancy, consisting of 18% in existing stock and the remaining 40% speculatively developed space.

While take up was lower in Q1 this year than in recent quarters, on an annual basis take up to April 2026 was still 6.6% higher than the 12 months to April 2025.

Prime take up accounted for 58% of activity in Q1, running ahead of secondary. Prime take up was led by speculative space (42,149sqm) followed by existing prime (32,438sqm) and precommitments (30,433sqm).

The Trade Coast was a standout over the quarter, with vacancy falling by 63,958sq m to 2.6%, down by 37% over Q1 and 45% over the year, as strong leasing activity and limited availability combined to drive one of the tightest conditions in the market. The precinct dominated take up in Q1, accounting for 44% of activity across a broad range of assets leased.

Knight Frank Partner, Research & Consulting Queensland, Jennelle Wilson, said the data points to a market where underlying demand is back to outpacing new supply.

“The slowdown in new speculative construction is allowing for the overhang of new supply to be absorbed quickly into 2026, bringing vacancy back down and reinforcing competition between tenants for high quality space,” she said.

“Across Brisbane we are seeing a breadth and depth of demand from tenants, across grades and functionality.”

Rental growth remained firm across all precincts in the quarter, with strong annual increases – of greater than 11% – recorded in key industrial hubs including the Trade Coast, South East and the North and Greater North.

Land values also continued to rise, particularly for sites sub-5,000sq m, reflecting ongoing competition for development-ready sites and limited availability of well-located industrial land.

On the investment side, transaction activity moderated over the quarter following a strong finish to 2025, with deals taking longer to complete as market sentiment shifted in response to global economic conditions and elevated funding costs.

Yields moved slightly higher across all asset grades over the quarter.

Knight Frank Partner, Head of Industrial Logistics Queensland, Mark Clifford said the shift in investment activity reflects capital market dynamics rather than any weakening in occupier fundamentals.

“Investor demand remains, particularly for well-leased, high-quality assets, but pricing expectations are adjusting in line with the current cost of capital,” he said.

“What we’re seeing is a period of recalibration, rather than retreat, with buyers remaining active but more measured in their approach.

“Looking ahead, supply constraints in several precincts are expected to persist, particularly where new development pipelines remain limited or slow to deliver.”

Related Articles