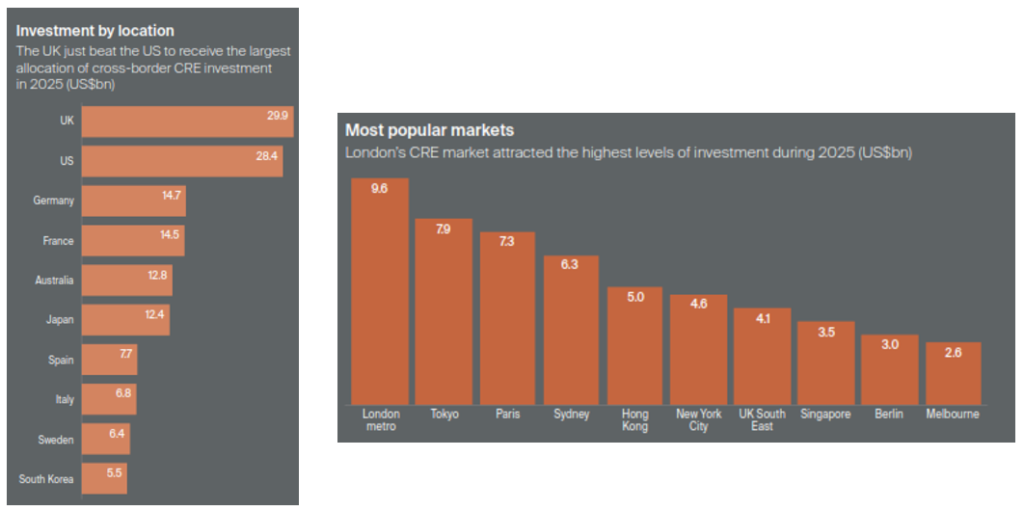

- The Wealth Report found cross-border investment in Australia was $US12.8 billion in 2025, behind the UK (US$29.9bn), the US (US$28.4bn), Germany (US$14.7bn) and France (US$14.5bn)

- Sydney attracted US$6.3 billion in investment, behind London metro (US$9.6bn), Tokyo (US$7.9bn) and Paris (US$7.3bn)

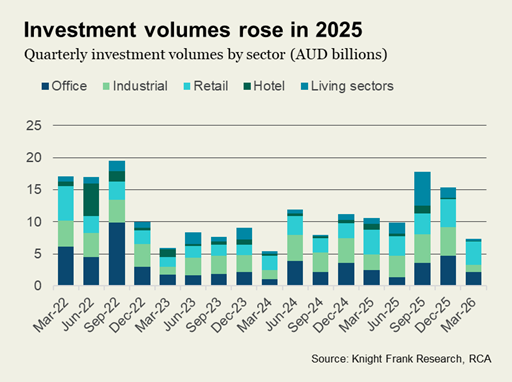

- Australian investment volumes in the CRE market rose strongly throughout 2025 with total annual investment volumes reaching A$53.6 billion — the third strongest on record

- Recent global instability has generated renewed uncertainty, and activity has slowed since February with some major investors pausing further deployment until the outlook stabilises

- Heightened geopolitical and economic volatility has reinforced Australia’s safe-haven appeal

Australia had the fifth largest allocation globally of cross-border commercial real estate (CRE) investment over 2025, with Sydney the fourth most popular city, according to Knight Frank’s landmark 20th edition of The Wealth Report.

The report found cross-border investment in Australia was $US12.8 billion in 2025, behind the UK (US$29.9bn), the US (US$28.4bn), Germany (US$14.7bn) and France (US$14.5bn). Sydney attracted US$6.3 billion in investment, behind London metro (US$9.6bn), Tokyo (US$7.9bn) and Paris (US$7.3bn).

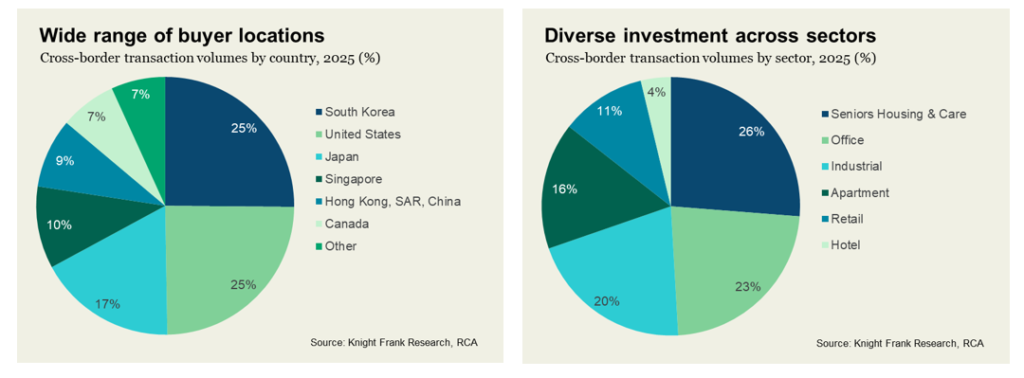

According to Knight Frank Australia research, cross-border capital in Australia was largely focused on Australia’s three largest capital cities – following Sydney (46% of cross-border purchases), Melbourne was the second most popular (21%), with Brisbane in third place (17%).

Over 2025 South Korea and the United States accounted for the largest share of buying activity in Australia (25% respectively), followed by Japan (17%), and Singapore (10%).

Asian investors were particularly active in the Australian market in 2025 as the market’s depth and relationship with the US made it a natural destination for capital seeking to diversify away from tariff-induced volatility across many other APAC regions.

Seniors Housing & Care was the largest sector for cross-border investment in Australia in 2025, mostly reflecting South Korea’s NPS purchase of Aveo — a retirement living operator. Outside of this transaction, cross-border investors were largely focused on the traditional sectors of office, retail and industrial in 2025.

While activity has slowed, Australia remains a sought-after destination for global capital

According to Knight Frank research, Australian investment volumes in the commercial real estate market rose strongly throughout 2025 with total annual investment volumes reaching A$53.6 billion — the third strongest on record. Investment volumes rose across all sectors, but the retail sector was the stand-out performer, with A$14.6 billion transacted.

Knight Frank Chief Economist Ben Burston said: “2025 saw a strong recovery in investment activity, with global markets emerging into a new growth cycle focused on supply and demand fundamentals and the opportunity to enter the market at attractive pricing.

“However, recent global instability has generated renewed uncertainty, and activity has slowed since February with some major investors pausing further deployment until the outlook stabilises.

“Preliminary data for Q1 2026 points to $7.3 billion in transactions — roughly 30% less than the volume recorded in Q1 2025 — underscoring the degree to which sentiment has shifted.

“As the year goes on and the shock fades, the trajectory driven by fundamentals will reassert with institutions and private investors seeking to identify opportunities to drive strong returns through income growth.

“This will draw them back to the traditional sectors including office markets, where sustained tenant demand for prime assets is generating positive absorption and diminishing new supply is driving accelerating rental growth in the major CBD markets.

“Amidst high and uncertain construction costs, investors are also more likely to focus their deployment on existing assets rather than new development. This also favours the traditional sectors over alternative asset classes given that they are more readily investable and new entrants can acquire large holdings stabilised assets without taking development risk relatively quickly.”

Knight Frank Chief Executive Officer James Patterson said: “Australia remains a sought-after destination for global capital, with cross-border investors responsible for 31% of total buying activity last year.

“Heightened geopolitical and economic volatility has reinforced Australia’s safe-haven appeal, underpinned by a rare combination of political stability, strong rule of law and market transparency that consistently places it among the world’s most liquid and accessible real estate markets.

“Global capital is also increasingly drawn to Australia’s improving fundamentals — strong population growth, resilient economic growth and structural undersupply across most asset classes present a compelling long-term outlook for investor returns in the years ahead.”

$144bn in institutional capital targets CRE re-entry globally as private wealth extends four-year dominance

Knight Frank’s The Wealth Report 2026 found investment in CRE globally grew by 12% over 2025 – a decent rise by any measure, and one that was reflected across all the major sectors.

It found that the appeal of more traditional sectors, including offices and retail, has experienced a revival, partly due to occupier demand returning to a sufficient level to push up rents in many locations. However, responses to Knight Frank’s Active Capital Survey also highlighted how thematic diversification and exposure remain on the agenda.

The Wealth Report identified a clear turning point for global commercial real estate as $144 billion of institutional capital prepares to re-enter the market in 2026.

The shift comes with private capital still firmly in the lead. Investors including high-net-worth-individuals (HNWIs) and family offices have now been the largest buyers of global CRE for four consecutive years, deploying US$464 billion in 2025 compared to US$347 billion from institutional investors.

In Australia, private capital remains an important component of the commercial market. Private investors had been the largest buyers of Australian CRE in 2023 (31%, $7.6 billion) and 2024 (29%, $8.9 billion). However, an improvement in market sentiment and growing evidence of a market recovery saw institutions (26%, $15.3 billion) take over from private capital (23%, $10.7 billion) as the biggest buyers of Australian CRE in 2025.

Knight Frank’s data shows capital is moving on fundamentals, rather than headlines. Despite current geopolitical risk and policy uncertainty, only 15% of survey respondents, representing US$1.4 trillion of assets under management, cite domestic politics as a key investment driver. Just 5% point to regulation and tax.

Globally, private capital’s advantage is becoming more pronounced. Speed of execution, flexible capital structures and a higher tolerance for risk are allowing it to transact earlier in the cycle and hold through volatility, widening the gap with more constrained and less nimble institutional buyers.

Related Articles