Richard Temlett, National Executive Director, Research

Charter Keck Cramer

There is real merit in making changes to the Capital Gains Tax (CGT) discount and Negative Gearing in Australia.

Given we have a national housing crisis, this debate needs to include the State and Territory Governments, and it is essential to also bring Stamp Duty, Land Tax and the various Foreign Investor Taxes & Charges into this discussion as all these taxes and charges are interrelated with each other.

Any changes need to have an evidence base, be properly explained to the public, protect the vulnerable, be phased in to avoid significant market distortions and must encourage new dwelling supply.

There has been a large amount of recent commentary about the potential changes to the Capital Gains Tax (CGT) and Negative Gearing that may be announced at the Federal Budget next month.

Charter Keck Cramer’s view is that this is a debate which deserves the fullest possible analysis — one that goes beyond changes to CGT or Negative Gearing at the Federal level and also examines the critical role that Stamp Duty and Land Tax reforms at the State and Territory level could play. These are deeply interconnected parts of the same system, and a comprehensive public conversation about all of them is both timely and necessary.

It is amazing to reflect that in 2019 the Labour Government proposed changes to CGT and Negative Gearing and it was a major reason for their election loss. These reforms were, and still are, incredibly politically sensitive. In 2026 the Labour Government is proposing similar changes to GCT and Negative Gearing and Charter Keck Cramer’s view is that it is highly likely that they will be made in May this year.

Much of this change in sentiment is driven by the change in the dynamics of the voter base. This has started to play out at the State level with various Governments attempting to make dramatic planning system changes to address the supply-side issues that previous Governments on both sides of the political divide have ignored for the last 20 years.

Charter Keck Cramer’s views are that we are at a seminal moment in time where we need to have a well-informed debate about the merits of these tax changes. This insight endeavours to start this discussion.

Key Concepts and Statistics

There are a number of key concepts and statistics that need to be explored to enable us as voters, as homeowners or renters, as parents and grandparents or as children and grandchildren to form a balanced view of the merits of some of these changes.

Some of these are summarised in this section of the article.

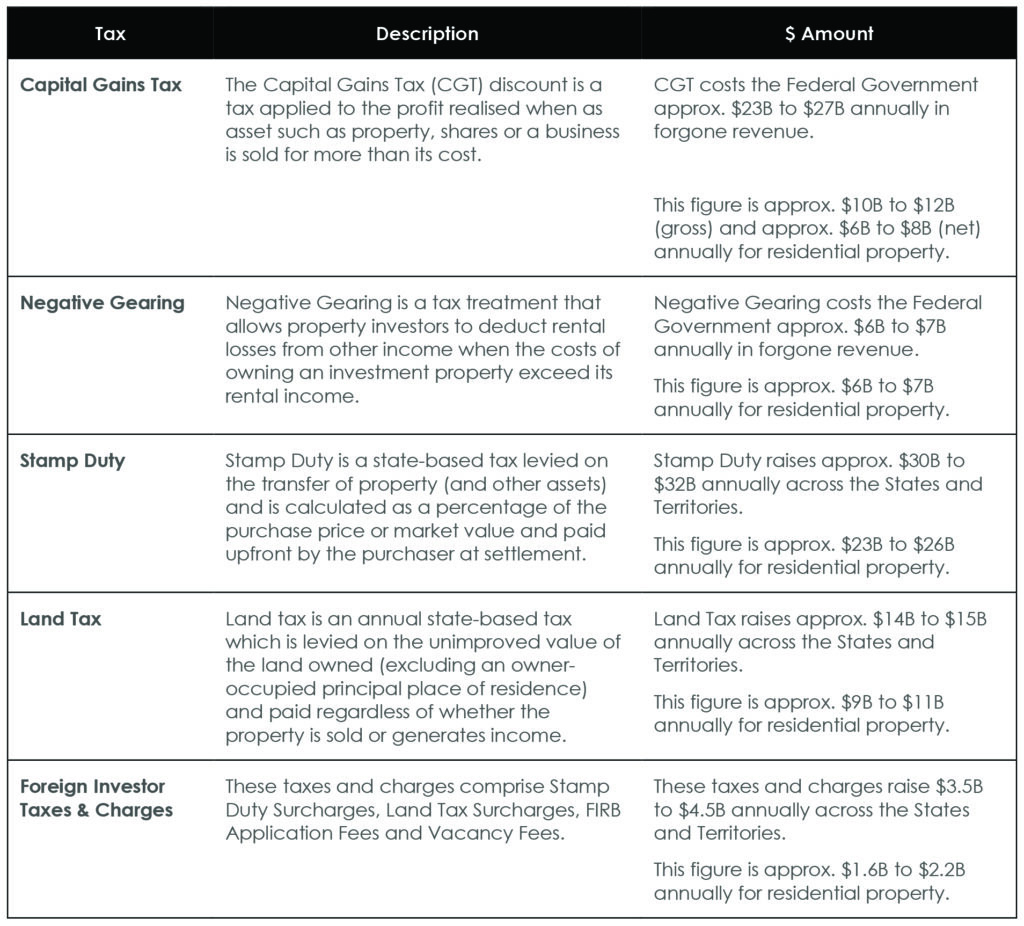

1.1 Taxes and Charges

The table below summarises the key taxes and charges that need to be considered in this debate.

Source: Treasury & Parliamentary Budget Office Estimates, ABS Tax Statistics, Budget Papers (various), Charter Keck Cramer.

NOTE: some of these figures are best estimates based on the documents and reports reviewed and used by the various levels of Government.

Our readers need to be aware that Australia has one of the most generous GCT and negative gearing systems in the world. Our research shows that countries that also offer various forms of CGT discounts include the USA, the UK, Canda and Japan whilst countries that also offer various forms of negative gearing concessions include Germany, Canada, Japan and Norway.

1.2 New vs Established Dwellings

On average, approx. 85-90% of investors purchase established dwellings in Australia whilst approx. 10-15% purchase new dwellings. This is a structural pattern rather than cyclical when the long-term averages are analysed. These figures are higher for high density apartments in various locations across our Capital Cities where investors comprise closer to approx. 30-50% of new dwellings.

Research shows that Foreign Investors represent approx. 2% to 3% of the total transactions each year (this peaked at 3% to 4% in the mid-2010s). Importantly though, Foreign Investors often account for approx. 30% – 40% of new dwellings each year in Australia which underscores their critical role in new housing supply.

1.3 Impact on Prices and Rents

There have been various studies carried out to show that there will in fact be a nominal impact on prices and rents of existing dwellings should the CGT or Negative Gearing settings be changed. These studies show that the impact to prices over the medium term will be an approx. decrease of -1% to -5% whilst to rents over the medium term it will be approx. increase of 1% to 4%.

This of course comes down to how the settings are changed but the public need not necessarily fear that prices of their existing homes will dramatically fall or that investors will completely exit the housing market and rents dramatically increase.

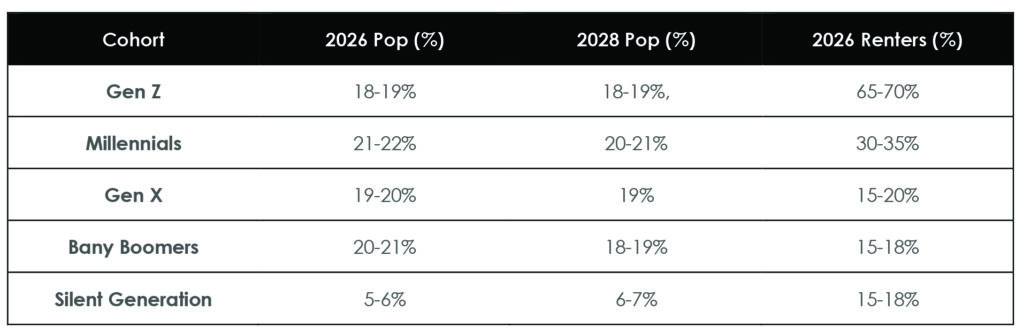

1.4 Current Changing Voter Base

The table below sets out a summary of the changing voter base across Australia.

Source: ABS, Statistica, Charter Keck Cramer.

At the time of the next Federal Election in 2028 approx. 38% – 40% of the voter base will comprise Gen Z and Millennials. Many of these voters will be renters and are at the coal face of the housing and costs of living crisis.

This shift from the Baby Boomer and Gen X voter base to the younger cohorts is a primary reason why Charter Keck Cramer has confidence that the next decade will see significant reforms which will be in response to a deeply dissatisfied, and now significant proportion, of the voter base who are not getting their needs met though the housing system.

Major Problems that aren’t going away

In 2026 we have a tax system that is badly out of date and simply not fit for purpose. Analysis of everyday Australians shows that almost every participant in the industry now has problems and none of these households are in fact being provided with the appropriate housing that meets their needs.

Younger generations are locked out of the housing market and are deeply dissatisfied that they are not being afforded the same opportunities as their parents and grandparents. At the other end of the spectrum are the older generations who are not able to downsize and age in place in appropriate forms of housing, nor are they able to live close to their children and grandchildren. Finally, they are also extremely worried about their inheritance and how that is going to be impacted by the current tax system.

Finally, we now have several State Governments who are deeply in debt and are not able to raise reliable forms of revenue on a consistent basis to assist with budget repair or assist the development industry will delivering new forms of housing supply.

The major culprit is of course Stamp Duty. This is one of the most inefficient taxes and distorts markets and buyer behaviour. It is also dependant on the property cycle, relies on transactions and is hence volatile.

By way of contrast, research shows that Land Tax is one of the most efficient taxes and not subject to the volatility of Stamp Duty. This is because it is levied on the value of the underlying land value of a property and not reliant on transactions or market turnover.

Finally, CGT and Negative Gearing benefit higher income households the most. This is because the benefits increase with marginal tax rates. The research also shows that these two tax concessions do encourage investors to bid up the prices of established dwellings often at the expense of first-home buyers.

Ideas for win-wins

As identified above, Charter Keck Cramer’s views are that over the next decade Australia will see dramatic reforms as the deeply dissatisfied voter base seek solutions and leadership from the officials they have elected. All sides of politics need to take heed of the major swings given the deeply dissatisfied segments of the voter market.

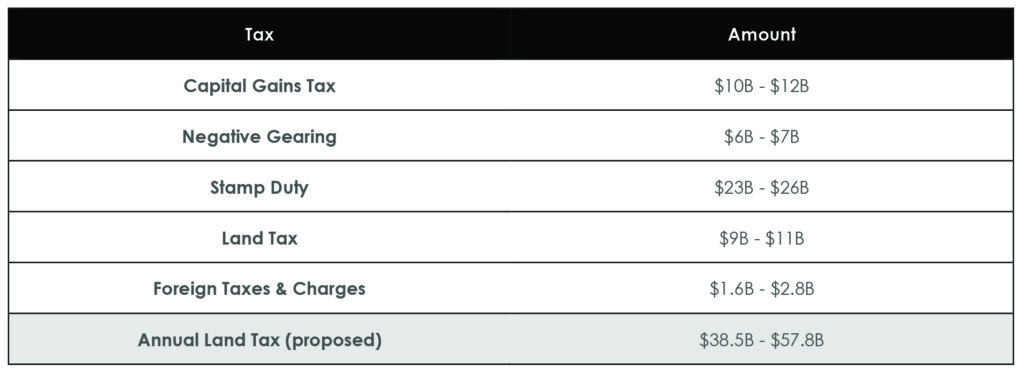

What are the numbers?

Our research shows that broadly, the total value of the unimproved residential land in Australia is approx. $7.7T.

Our high-level calculations show that a broad-based annual Land Tax applied to all residential property across Australia could raise approx. $38.5B to $57.8B per year. This is based on a 0.5% or 0.75% annual tax rate on the estimated $7.7T value of unimproved residential land in Australia.

The table below sets out a summary of the current numbers as they relate to housing in Australia. We have included the proposed numbers for an annual Land Tax for the sake of comparison.

Land Tax for the sake of comparison.

Source: Treasury & Parliamentary Budget Office Estimates, ABS Tax Statistics, Budget Papers (various), Charter Keck Cramer.

NOTE: some of these figures are best estimates based on the documents and reports reviewed and used by the various levels of Government.

Whilst Stamp Duty is a significant source of revenue for the States and Territories, it is important to understand that a broad-based annual Land Tax could in fact replace this source of revenue. Subject to the various changes that could be made, the revenue that could potentially be raised from these reforms could be used for various solutions which include:

- Broader tax reform.

- Infrastructure delivery.

- Social and affordable housing delivery.

- Budget repair.

- Subsiding the costs of delivery to make new housing feasible.

What are the non-negotiables?

Any changes need to be designed so as to avoid crashing the markets. They don’t need to be blunt but rather stepped changes, grandfathered and better targeted to achieving the goals of new housing supply. For example, negative gearing could be restricted to new housing supply and this could be paired with supply-side incentives which encourages net housing additions.

Governments must not do anything to negatively impact new supply at this point in the cycle. This will undermine the National Housing Accord targets further. In fact, there is an argument that at this point in the cycle, and to offset the dramatic increase in the costs of delivery, the incentives could be increased to stimulate new housing supply.

Government must also not do anything with retrospective changes as this undermines trust. Finally, Government must be aware of “double taxation” for various transactions that have already occurred.

Replacing Stamp Duty with Land Tax – A pragmatic idea that works

A major idea that ought to be fully explored is for the Federal Government to work with the States and Territories to replace Stamp Duty with a broad-based annual Land Tax. To do this, both the CGT and Negative Gearing could be reformed with the revenue from GCT and Negative gearing used to subsize this transition over a period of 10 to 20 years.

Replacing Stamp Duty with Land Tax will lead to major productivity gains, better utilisation of housing stock and more stable revenue for governments. It’s a win-win for everyone. This reform aligns with the recommendations by Dr Ken Henry and are also in line with OECD best practice principles.

These reforms need to be implemented over 10 to 20 years, via a stepped change through various market cycles. If designed correctly, the figures set out above have attempted to show that there is the possibility for these changes to minimise any distortions to the market and could even be revenue neutral.

Final Thoughts

This article has highlighted that the current tax settings as they apply to the housing market are not working as efficiently as they could be. We are at a moment in time where we need to have a fully informed debate about how these settings could be changed so that the system is fit for purpose and produces better outcomes for all residents of Australia.

Given the change in voter base, our views are that significant changes are inevitable given the dissatisfaction with the current Federal, State and Local policies in addressing both the housing crisis as well as the cost of living crisis in Australia.

Now is the time to act and Charter Keck Cramer is here to support these debates with thought leadership.

Related Articles