Sydney’s Multi-Speed Office Market Gains Pace as Demand for Centrally-located Assets Bucks 30-Year Trend

29 March 2023

The 2023 ‘Spotlight: Flight to Quality Report’, released by leading agency Savills Australia, has revealed growing strength within Sydney’s premium office market, with a three-year cumulative increase in net absorption totalling around 12.3% of premium office stock.

While the report revealed continuation of some established commercial office market trends, a new growing demand divergence between asset locations in Sydney’s CBD is defying the market conventions of the last 30 years.

Office assets within Sydney CBD’s Midtown, Southern and Western precincts are experiencing declining net take-up, with office stock in each of these precincts displaying negative net absorption in the three years to 2022.

According to Savills, continued robust demand for premium office space reflects the ongoing ‘flight to quality’ trend, with the relatively tightly-held market displaying no signs of weakening despite slowing global economic growth, high inflation, rising interest rates and a shift in working patterns catalysed by the pandemic.

Driven by structural changes to working environments and relatively low exposure to leasing risk, this steady demand for premium office space in Sydney and other major office markets in Australia is set to continue.

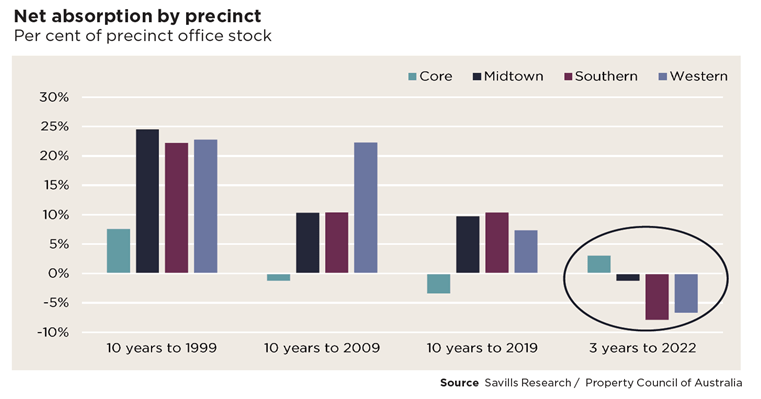

Sydney CBD: Rising Core Take-up Leads to Decline in Demand for Peripheral Assets

Savills’ report has highlighted that net absorption in the Midtown, Southern, Western precincts of Sydney’s CBD have declined in contrast to rising Core take-up. This bucks the trend of the last three decades, which saw strong take-up in these precincts due to the relative affordability of leasing space in these areas and development of underutilised space.

Net absorption in the Core was historically weak from 1989 to 2019, averaging just 1% over this period and with negative absorption from 1999 to 2019. By contrast, take-up in the Midtown, Southern, and particularly Western precincts grew strongly over this three-decade period, increasing by an average of between 14.3% and 17.5% of precinct office stock.

Conversely, during 2021-2022 these precincts have experienced rapid decline in absorption with the Western CBD suffering a -40,700 sq.m decrease and Southern CBD reporting a -25,000 sq.m decrease.

Net absorption in the Sydney CBD core however increased by 101,100 sq.m in 2021-2022.

”With demand for premium office space in core locations growing strongly, premium office assets in core locations remain in favour with investors due to their relatively high rental growth prospects” said Chris Naughtin, National Director, Capital Markets – Research at Savills Australia.

He noted that a relatively strong occupier market outlook for centrally-located prime assets will drive an investor rotation into Core assets and out of non-Core assets, potentially supporting a rebound in deal activity in H2 2023 as the interest rate outlook becomes clearer.

Savills asserts that assets in central locations with strong transport links will continue to outperform, alongside newer, higher quality office space that help support business continuity, meet environmental and sustainability mandates, cater to the changes in work patterns, and allow employers to compete for talent.

In many cases, spaces are undergoing whole floor fitouts to fulfil these tenant requirements, says Tom Mott, State Director – Office Leasing NSW at Savills.

“Across the Sydney CBD, there is no fewer than 27 whole floor spec fitouts underway, representing 33,516sqm of total NLA, which is unprecedented.

“This means that of all Prime Grade whole floors available in the following six months, 11.7% have spec fit outs in them, equating to 9.5% of the total whole floor Prime grade NLA vacancy between now and September,” Mr Mott concluded.

Sydney Prime Assets to Continue Outperforming

According to Savills, prime assets are beginning to materially outperform the secondary market in terms of capital value growth and total investment returns, following the broad-based rebound in capital growth following the pandemic downturn. This divergence in performance is already occurring and likely to continue.

Stronger demand for Core assets, highlighted by Savills, is underpinned by major institutional investors repositioning their portfolios to reduce leasing risk. While demand trends over the 2020-22 period have been heavily impacted by COVID-19, the rebound in demand for office space has been heavily skewed towards the Core where net absorption has increased by 101,100 sqm over these two years.

Multi-Speed Market Continues with Growing Divergence in Demand for Office Space

Alongside a marked divergence in asset location, Savills’ Flight to Quality Report highlighted a concentrated demand for premium office space across most of Australia’s capitals, whilst demand for secondary stock decreases.

Savills forecasts that this is likely to continue, supported by a slower economic growth outlook increasing investment in assets with lower leasing risk. Stronger emphasis on amenity, location, and green credentials are also expected to drive premium take-up.

From 2013-22, national net absorption in the premium segment averaged c.132,400 sqm – 4.9% of premium office stock – per year, compared with 2.5% of stock per year over the decade prior. Over the 2013-22 period, net absorption in the A grade segment has remained positive yet steadily slowed, while net absorption in the secondary market has declined by 1.4% on average per year.

This shows a significant divergence between prime and secondary take-up.

“While there is a lot of talk about ‘flight to quality’ as a post-COVID office trend, it is important to recognise this divergence is nothing new,” Mr Naughtin said.

“We’ve seen the secondary-grade office market slow consistently over the past decade and the pandemic has simply continued and to a degree, accelerated this trend.”

Flight to Quality Continuing Amid Growing Green Wishlist

Savills’ research revealed that robust demand for premium office space has continued over the last decade, catalysed by a spate of new office developments that have resulted in higher availability. The premium segment’s share of total office stock has increased by 5.5 percentage points (around 75%) during this period, growing from representing 7.4% of total commercial office supply in January 2012 to 12.9% in January 2023.

A cumulative increase in net absorption since H1 2020 has totalled 12.3% of premium office stock. From 2013-22, net absorption in the national premium segment averaged 4.9% of premium office stock per year, compared with 2.5% per year over the decade prior.

The increasing emphasis that investors and occupiers are placing on green credentials is leading to a significant green price premium. Green assets are commanding higher rents and capital values – beneficial for owners and attractive for prospective investors.

Structural trends and changes to working patterns in the wake of the pandemic have also led to employers recalibrating their working environments, seeking to attract and retain talent amidst a tight labour market.

“The shift in working patterns towards a hybrid model has put pressure on employers to deliver premium workplaces that ‘earn the commute’ and boast strong environmental credentials,” Mr Naughtin said.

Increasing emphasis on green credentials from both investors and tenants remains another key driver of the ‘fight to quality’ trend as occupants seek to align their workplaces with their corporate sustainability targets.

According to Savills World Research, on average, just 28% of total stock in the top 20 cities is green certified, showing a strong demand relative to limited supply. This is driving a material premium for highly rated green assets, both from a capital value and rental income perspective.

Mr Naughtin states that “sustainable certifications have made premium office spaces even more desirable, both to employers and their staff. This reflects a promising trend for investors, will lead to further premium green developments down the line, and unlocks the potential to redevelop and reposition secondary stock.”

Investment in Premium to Rise

Savills forecasts investor demand for Australian premium commercial office space will remain strong despite slowing global growth, high inflation, and rising interest rates. While the Australian economy is expected to avoid recession in 2023, economic growth is likely to slow materially, and Savills warns that a softening in labour market conditions – both domestically and globally – may increase leasing risk in some markets.

Premium markets remain relatively tightly held and less exposed to leasing risk. Nationally, the premium vacancy rate is just 8.7% compared to 13.3% for A grade and 14.7% for secondary office space.

“Some investors will continue to wait for the impact of rising interest to wash through valuations, but low leverage among many major investors means increased rates pose limited systemic risks to the commercial property sector,” he said.

The increasing focus on office assets’ green credentials, better amenities and higher environmental benchmarks will require the vast majority of office stock to be retrofitted or repurposed. While this represents a significant opportunity for value-add investors, current inflation rates and strong growth in material and labour costs may make many such projects cost-prohibitive in the short-term.

Related Articles