Global Data Centre Market Is Projected to Reach US$4 Trillion by 2030, with 18% CAGR Growth

9 April 2025

- Knight Frank latest Global Data Centres Report found global data centre growth is projected to reach US$4 trillion by 2030, with 18% CAGR growth

- Asia-Pacific leads global data centre investment, capturing US$15.5 billion in 2024, and accounting for 70% of cross-border investment

- Australia was the second top investment location for capital in 2024 with $6.7 billion, behind the United States at $14.6 billion

- The Knight Frank report found Australia’s data centre market has gained significant momentum following the recent US ruling that grants the country privileged access to Nvidia AI chips. As one of only four nations in APAC exempt from any export restrictions, Australia now holds a strategic advantage in the AI race

- Traditionally viewed as a secondary market to Sydney, Melbourne is rising as a key data centre hub as power availability becomes increasingly difficult in Sydney and land scarcity intensifies

Knight Frank has published its latest Global Data Centres Report, projecting market growth at a compound annual growth rate (CAGR) of 18% over the next five years, with the market expected to reach US$4 trillion by 2030.

The analysis forecasts capital expenditure exceeding US$286 billion by 2027 as operators respond to mounting demand for AI-optimised infrastructure, cloud services, and enterprise digital initiatives. The research examines critical factors shaping data centre capacity planning and operational strategies across global markets.

Key Findings

- Capacity Growth: Global data centre capacity is projected to increase by 46% over the next two years, adding approximately 20,828 megawatts (MW). By 2030, capacity could expand by 177%, driven by escalating demand for AI and enterprise digital transformation.

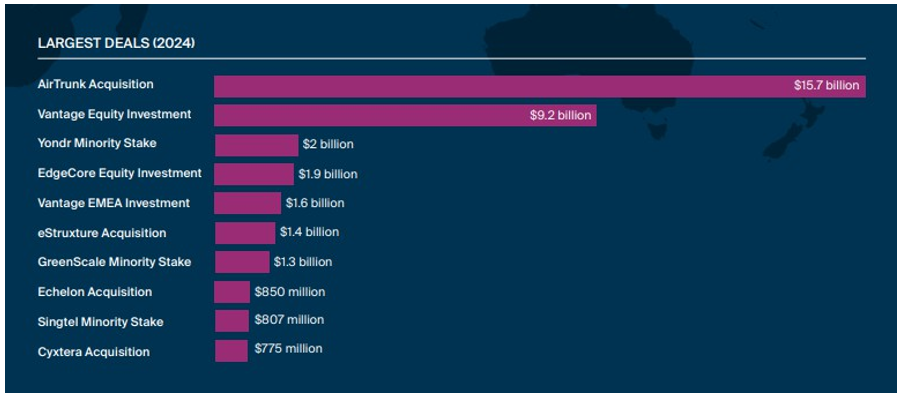

- Transaction Volumes: Following a 36% decline in transaction volumes in 2023 due to global interest rate hikes, the market rebounded strongly in 2024. Global transaction volumes grew 118% to reach U$31.8 billion across single-asset purchases, portfolio acquisitions, redevelopment opportunities, and development site sales.

- Average Transaction Value: Globally, the average real estate transaction value for data centres rose to US$75.4 million in 2024, up 15% from 2023 and 44% higher than pre-COVID levels in 2019. Since 2019, average transaction values have grown at a CAGR of 7.5%.

Capital Flows: APAC Leads Global Investment Volumes In 2024

Asia-Pacific (APAC) emerged as the leading global investment destination for data centres in 2024, capturing US$15.5 billion in cross-border investment, more than any other region worldwide. This influx of investment demonstrates APAC’s growing strategic importance in the global digital infrastructure landscape.

APAC Growth Projections Through 2026

Building on this investment momentum, APAC is forecast to add 4,174 MW of capacity (a 32% increase) by 2027, supported by planned investments totalling US$58.7 billion over this two-year period. This expansion spans diverse markets from established hubs such as Tokyo, Japan to rapidly developing locations such as Johor, Malaysia, where major cloud providers are securing strategic sites to meet escalating regional demand.

Key data centre markets in APAC:

- Melbourne, Australia: A major shift towards ultra-high-density deployments is redefining the city’s data centre landscape. AI workloads require significantly more power, pushing rack densities from 30 to 40kW to over 80kW. This has intensified competition for high-density- ready colocation space, with operators racing to integrate liquid cooling and power distribution upgrades.

- Mumbai, India: AWS is transforming Mumbai’s data centre market by scaling through colocation rather than self-building. Instead of acquiring land and constructing its own facilities, AWS is leasing large amounts of capacity from third-party operators. This approach has made Mumbai one of the most competitive leasing markets in APAC.

- Tokyo, Japan: This key APAC hub is poised for 25% capacity growth (295 MW) over the next two years, supported by US$4.1 billion in investment. Japan’s strategic location, stable power infrastructure, and expanding cloud service requirements continue to drive steady market development despite land constraints.

- Johor, Malaysia: Positioned for significant expansion with 85% capacity growth (335 MW) over the next two years, backed by US$4.7 billion in investment. Johor’s strategic location adjacent to Singapore, coupled with favourable government incentives and lower operational costs, establishes it as a viable alternative for hyperscale expansion.

- Singapore: With vacancy rates below 1%, the main liquidity of transactions has shifted towards smaller rack deals despite Singapore’s standing as a large-scale market. These fractional capacity deals have surged in pricing, with some operators securing pricing exceeding US$1,000. Investors and operators continue to recognise the profitability of these small-scale transactions, with colocation providers rapidly leasing out available capacity at premium prices.

- Bangkok, Thailand: With land and power costs significantly lower than in other Tier 1 APAC cities, hyperscalers can achieve rapid deployment while maintaining operational control. However, despite the market’s potential to become a gigawatt-scale hub, the extent to which colocation will play a role remains uncertain.

Stephen Beard, Global Head of Data Centres at Knight Frank says, “The global data centre industry is undergoing rapid transformation, with hyperscaler and colocation providers prioritising markets that offer access to power, robust connectivity, and a favourable regulatory environment. We are increasingly seeing sustainability considerations shaping investment strategies, with an increasing focus on renewable energy adoption and energy-efficient design. Real estate investors and developers are positioning themselves to capitalise on this demand, with an emphasis on acquiring strategically located land and securing long-term power agreements.

“As global capital races to capture the next wave of digital infrastructure growth, the competition for prime development sites, particularly in power-constrained locations, will intensify. Industry stakeholders must navigate regulatory complexities, power availability concerns, and sustainability requirements to remain competitive in this high-growth sector. Operators, investors, policymakers, and partners, each have a role to play in shaping this future. The task ahead is to build infrastructure that not only supports innovation but also safeguards sustainability, security, and equity.”

Fred Fitzalan-Howard, Head of Data Centres, APAC, adds, “The region’s data centre market is positioned for substantial growth, driven by increasing investor interest across both tier 1 and emerging tier 2 markets. Over the next three years, the APAC data centre market is expected to add approximately 8GW of new capacity, with 25% dedicated to AI workloads, lower than the global average due to the region’s Tier 2 or Tier 3 status under U.S. AI diffusion rules. This rollout represents a capital expenditure of US$24 billion and a real estate requirement of 20 to 30 million square feet.

While AI deployments in APAC are still in their early stages compared with the U.S. and Europe, the region presents significant opportunities for growth. Pilot projects and initial investments are laying the foundation for broader AI infrastructure rollouts. However, addressing varied regulatory frameworks and adapting to U.S. export controls on AI chips remain essential factors in maximising APAC’s opportunities in this rapidly evolving sector.”

Data Centres in Australia

The Knight Frank report found Australia’s data centre market has gained significant momentum following the recent U.S. ruling that grants the country privileged access to Nvidia AI chips. As one of only four nations in APAC exempt from any export restrictions, Australia now holds a strategic advantage in the AI race, attracting increased investment from hyperscalers and enterprises looking to deploy next-generation infrastructure. With restrictions tightening in other APAC regions, Melbourne is emerging as a key location for AI-driven data centre growth.

Traditionally viewed as a secondary market to Sydney, Melbourne is rising as a key data centre hub as power availability becomes increasingly difficult in Sydney and land scarcity intensifies. The state of Victoria is also taking a more proactive approach to approving data centre applications versus New South Wales. Hyperscalers and colocation providers are accelerating large-scale investments in Melbourne, tapping into its growing AI and cloud demand to establish high[1]performance computing infrastructure. A major shift towards ultra-high[1]density deployments is now redefining the city’s data centre landscape. AI workloads require significantly more power, pushing rack densities from 30-40kW to over 80kW. This has intensified competition for high[1]density-ready colocation space, with operators racing to integrate liquid cooling and power distribution upgrades. As AI adoption continues to reshape infrastructure needs, Melbourne is rapidly transforming into a critical destination for next[1]generation digital infrastructure in APAC.

Knight Frank Head of Industrial Investments Angus Klem said buyer demand for data centres was only strengthening in Australia.

“The purchase of AirTrunk, which develops and operates large-scale data centre campuses across the Asia-Pacific region, by Blackstone and the Canada Pension Plan Investment Board last year, was the largest data centre transaction globally in 2024,” he said. “It cemented data centres as a major growth sector for Australia, and momentum has only been building since then.

“We have seen strong investment from overseas investors, with Australia the second top investment location globally for data centres last year. However, we are also seeing domestic buyers doing the ground work and readying themselves to invest, and with capital competing for opportunities, we will continue to see rapid growth in the data centre space.

“Sydney has seen significant activity in the data centre space, and while the focus now looks to be turning to Melbourne, we are also seeing Perth gain more traction and over the coming years, the momentum in the data centres sector will flow through to every Australian capital city.”

Related Articles