Foreign investors take most prominent share of commercial property market, driving transactions to $11.5 billion in 1H 2024

10 July 2024

AUSTRALIA, 10 July 2024 – Investment into Australia’s office, retail and industrial markets topped $7 billion in Q2 2024 as foreign investors made major office acquisitions and industrial investment continued to surge, according to preliminary sales volumes figures released by JLL Research.

Indicative figures for 2Q 2024 reveal that combined investment in the three key commercial sectors of office, retail and industrial was 60% higher than 1Q 2024 and double that of Q2 2023. This was delivered by strong investment in the office ($2.7 billion) and industrial sectors ($3 billion), which combined accounted for 80% of the 2Q total.

JLL Research found that office sales had increased from a low base in 1Q to 2Q in 2024 following large institutional sales in Sydney – of 55 Pitt Street and 5 Martin Place; 240 Queen Street in Brisbane and 40 Miller Street, North Sydney.

The rebound in foreign investment in Q2 resulted in offshore buyers taking the largest share of Australian commercial property market sales, after spending $2.8 billion in the six months to June 30 compared to $3.2 billion for the full year 2023.

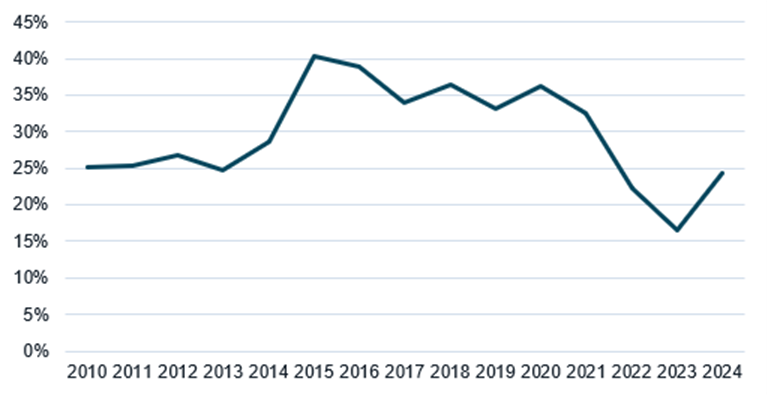

JLL Research estimates that foreign investors have accounted for 24% of total investment sales to date in 2024, up from a low of 16% in 2023 but still below the 10-year average of 32%.

Private capital was also a major contributor to deal volumes ($2.25 billion), followed by superannuation funds ($1.96 billion).

Office Retail Industrial Total 2Q 2023 $594 million $1.3 billion $1.6 billion $3.5 billion 2Q 2024 $2.7 billion $1.3 billion $3.0 billion $7.1 billion 1H 2023 $2.6 billion $2.5 billion $3.1 billion $8.3 billion 1H 2024 $4.0 billion $1.9 billion $5.5 billion $11.5 billion

“We’re encouraged by the activity in the first half and that it reflects the start of a rebound in capital markets activity. Given the typical skew towards the second half of the full year calendar (60%), we estimate approximately $28 billion of total volume in 2024, which would be up notably from $19.4 billion in 2023 and close to the long term average of around $31 billion,” said JLL’s Head of Capital Markets – Australia and New Zealand, Luke Billiau.

He said the jump in sales in the second quarter partly reflected the ongoing appetite for industrial assets, more price discovery, and updated valuations in the office sector that generally assisted with closing the bid-ask gap.

“We need to start getting comfortable with uncertainty. The global macro environment certainly still has some challenges that are weighing on investors. Still, risks are being priced in and more groups are starting to look to Australia for stability, growth and interesting investment opportunities.

Mr Billiau said commercial property sales in the 1H were driven by Australian listed and unlisted funds divesting assets.

He said offshore investors took a $2.1 billion plunge into the Australian market and have started to make significant moves including the following sales:

- Mitsui Fudosan acquiring two-thirds stake in Mirvac’s 55 Pitt Street office development for $1.3 billion;

- Keppel REIT acquiring a 50% stake in 255 George Street for $363.8 million (Q1 transaction);

- Barings acquired an office building at 40 Miller Street in North Sydney for $145 million;

- Barings also acquired a share in an industrial portfolio from Goodman Group for $780 million in partnership with REST.

“Although retail investment was somewhat subdued in 1H23, the outlook remains positive, given a change in institutional sentiment towards the sector and a pipeline of transactions that will likely contribute to volume in the second half of the year,” he said.

Figure 1: Offshore investor share of total Australian transactions

Source: JLL Research

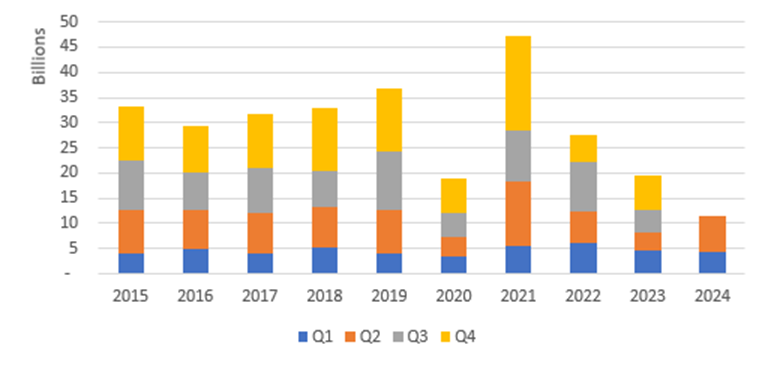

Figure 2: Transaction volume by quarter

Source: JLL Research

Related Articles