Australia’s Build-to-Rent sector gaining momentum amid tight rental market

22 March 2023

Australia’s fierce rental market is proving a tailwind for the Build to Rent (BTR) sector, with the completion and lease-up of several developments in late-2022, and more projects emerging by the day.

JLL experts see the sector gaining momentum in 2023, with rental conditions unlikely to improve in the medium term and the BTR concept gaining popularity.

However, rental affordability will be critical in the sector’s continued development, while developers face the twin challenges of rising construction and finance costs.

“Despite the challenges for BTR developers, they still have a significant competitive advantage over build-to-sell developers in not having a lengthy selling period where construction and finance costs are not locked in,” noted Leigh Warner, JLL Head of Residential Research – Australia.

“This has meant that BTR operators have been in a strong position to bid for major high-density development sites over the past year or so. This has been particularly evident in Melbourne where more sites have been available.”

Another potential opportunity for BTR developers in 2023 may be the availability of capital as economic pessimism abroad makes Australia’s comparatively insulated outlook appear even more attractive. The prospect of continuing strong residential rental demand should coax overseas investors to boost their allocation to Australian BTR where they can.

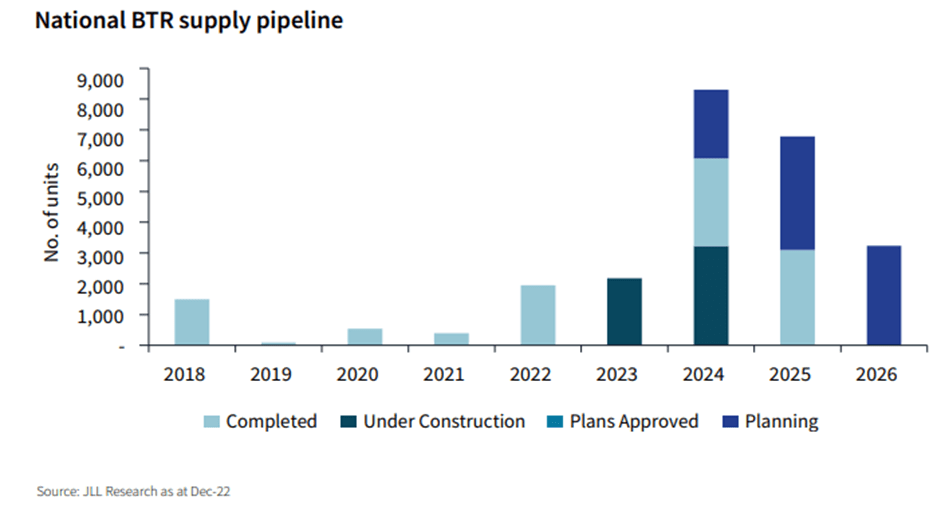

Despite the challenges facing BTR developers over 2022, the size of the overall supply pipeline between 2023 and 2025 has expanded. At end 2022, there were a total of 20,515 BTR apartments in the pipeline for this period, which compares to around 13,600 a year earlier.

The number of apartments under construction (UC) fell slightly in 4Q22 due to several completions, but there were 5,413 units remaining UC at the end of the year plus an additional 5,944 with planning approval (PA) and 9,158 in earlier planning stages.

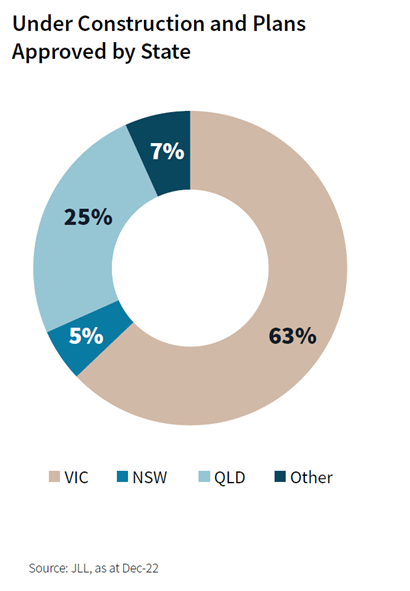

Of those UC or PA, Melbourne still dominates the pipeline, with around 63% of planned supply. Interest in Brisbane (25%) has grown significantly in 2022 and this was the second highest share, but the challenges of making projects work in Sydney are reflected in a lower share of the pipeline.

Looking at both operational and pipeline projects, Home has the largest pipeline of major institutional players with 2,288 apartments, followed by Mirvac’s Liv pipeline (2,199) and Greystar (1,944).

JLL’s Head of Alternative Investments – Australia, Noral Wild said, “Leasing interest has generally been very strong for the new units that completed in 2022, along with other existing BTR developments, reflecting the tight rental market conditions.

“We anticipate site acquisition opportunities to increase in 2023 as vendor expectations adjust to the reality that higher interest rates are affecting demand and pricing for sites (from all sectors). This adjustment will likely see the number of opportunities increase for those well capitalised BTR operators who are in a position to build their pipeline and market share, perhaps in the second half of the year,” said Ms Wild.

Key trends for the BTR sector in 2023 include:

- A clearer picture via greater operational data and analysis of project leasing metrics, rents and the types of amenities and features that work best.

- New players emerging in the BTR space.

- Even greater government support through taxation measures and planning regulation in the face of rising political pressure to address imbalances in the rental market.

- A wider geographic focus for new developments.

- Site acquisition opportunities for BTR operators in the second half as vendor expectations adjust to the reality that higher interest rates mean much lower demand and prices.

Related Articles