AI-Driven Data Centre Boom Intensifies Competition for Construction Talent Across Australia and New Zealand

10 July 2026

Australia and New Zealand facing capacity crunch driven by competing demands and preparation for 2032 Brisbane Olympics and Paralympic Games

A new report published today by global programme manager, Turner & Townsend, reveals that rapid growth in AI infrastructure and data centre development is intensifying labour shortages across Australia and New Zealand’s construction sector. Increased demand from data centres, health and defence projects, and the 2032 Brisbane Olympic and Paralympic Games’ preparation is creating fierce competition for skilled workers and driving the adoption of new delivery approaches.

Now in its 17th year, Turner & Townsend’s Global Construction Market Intelligence report represents the definitive analysis of the global construction industry, with data gathered from 112 markets across 44 countries.

Driven by AI adoption and the push for data sovereignty, data centres have become one of the fastest-growing sectors across Australia and New Zealand, placing the region at the start of a sustained data centre expansion cycle that is expected to build momentum into 2027. At the same time, rising geopolitical uncertainty is driving increased defence investment, including new opportunities linked to the AUKUS partnership between Australia, the United Kingdom and the United States. Together with the preparations for the Brisbane 2032 Olympic and Paralympic Games, these major projects are placing increasing pressure on supply chains and intensifying workforce shortages.

Key findings from the report include:

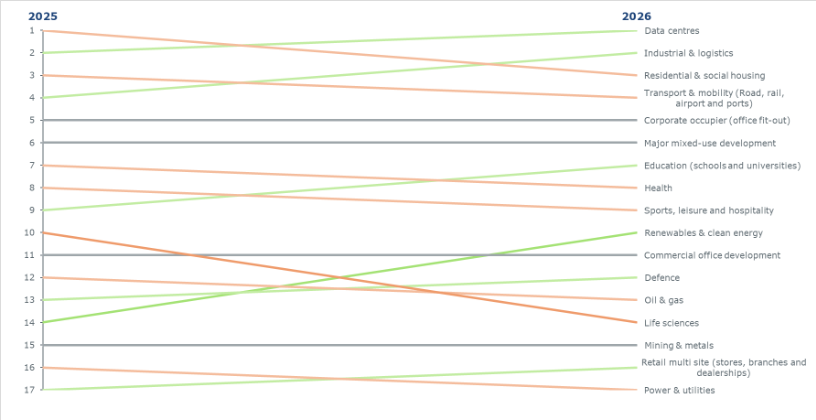

- Health is the strongest performing sector across Australia and New Zealand, followed by transport and data centres, with defence also performing strongly

- More traditional sectors, such as commercial office development and residential, continue to face weaker market conditions

- Data centres are the top performing sector in both Sydney and Melbourne

- Brisbane is expected to become a major construction hotspot ahead of the 2032 Olympics, driving construction cost inflation to 7.2% in 2026

- Construction cost inflation across Australia and New Zealand is forecast to reach 5.4% in 2026,

before easing to 4.9% in 2027 - Brisbane is expected to record the highest construction cost inflation in the region, rising to 7.5% in 2027.

Perth is forecast to reach 6.5% in 2026 before easing to 5.5% in 2027, while Sydney and Adelaide are forecast to see inflation of 5.5% in 2026 - Adelaide is forecast to experience an increase in inflation by more than 2% between 2025 and 2026,

while Perth is expected to increase by 2.6% - Australia and New Zealand remain the most labour constrained markets globally, with labour shortages reported across 100% of cities surveyed

Recent trends have created a two-speed construction market, both in terms of sectors and geography. Data centres, defence and health are all performing strongly, while office development and residential construction face tougher conditions. Regional performance is also diverging, with Brisbane and Perth leading the outlook for non-residential construction activity, and Adelaide gaining momentum. While Sydney and Melbourne benefit from strong data centre investment, Auckland is experiencing more subdued conditions, reflecting a weaker pipeline.

Despite the volatility created by recent geopolitical events, construction input costs have stabilised over the past year, as the increased supply chain resilience built up in the sector since the COVID-19 pandemic has limited the impacts from recent global volatility. Construction cost drivers are becoming more localised, sector-specific, and structurally embedded, rather than driven by international shocks.

While renewed pressure on material costs remains a key risk, labour availability continues to be the primary driver of construction cost escalation across Australia and New Zealand. The region is the most labour-constrained construction market globally, with 100% of markets surveyed reporting labour shortages. Growing demand from data centres, defence, health and major infrastructure programmes is intensifying competition for skilled workers, particularly in specialist trades critical to complex projects. This comes as 71% of markets report labour shortages, with markets in the European Union (93%) and North America (79%) reporting shortages above this average.

Rapid growth in data centre investment is helping to offset weaker demand from traditional private-sector sectors, but it is also placing additional pressure on an already constrained workforce. Data centres are now the most capacity-constrained sector in Australia and New Zealand, with around 67% of markets reporting tightening contractor capacity. The sector’s continued expansion is increasing demand for highly specialised skills, particularly across mechanical, electrical and plumbing (MEP) trades, where 83% of markets report shortages in the region.

Brisbane is expected to become a construction hotspot in the run-up to the 2032 Olympic and Paralympic Games and, together with significant health infrastructure investment in the region, this is expected to drive costs up by 7.2% in 2026. The city is consequently expected to see the highest inflation in construction costs across Australia and New Zealand this year, followed by Perth at 6.5%, and Adelaide and Sydney, both at 5.5%.

Tiffany Emmett, Project Director and Head of Construction Economics for Australia and New Zealand at Turner & Townsend, said: “The global construction market is shifting, and new dynamics are reshaping the key drivers of cost performance. Demand is increasingly uneven and concentrated on AI-driven sectors like data centres, while broader labour constraints, supply chain risks and geopolitical uncertainties are becoming more pronounced.

“There is a real risk that growth in the pool of skilled labour needed to deliver data centres won’t keep pace with demand in Australia and New Zealand. AI has the potential to create significant opportunities across the construction sector, but only if the industry can attract, train and retain the workforce needed to support this growth. At the same time, recent geopolitical developments and rising energy prices are increasing the risk of renewed input cost pressures, although impacts are likely to vary by geography, sector and supply chain exposure.

“More broadly, the region is seeing increasing competition for skilled labour, with projects related to the Brisbane Olympics up against health projects in Queensland, as well as a data centre wave across the country as a whole, and increased investment in defence.”

“Clients with global portfolios should use this opportunity to review international programmes to ensure investment is prioritised according to local market conditions. It is no longer simply a question of relative cost, as factors such as labour availability, interest rates, supply chain capacity and digital maturity are playing an increasingly important role in successful project delivery.”

Ranking of top markets in ANZ

Market Region Ranking (/112 markets) Cost per sqm (USD) 2025 construction cost inflation (%) 2026 construction cost inflation (%) Wages / hour (USD) Wages / hour (AUD/NZD*) Brisbane Australia 45 3,828.4 6.2 7.2 72.4 105.3 Sydney Australia 47 3,708.7 3.7 5.5 73.4 106.9 Perth Australia 56 3,436.1 3.9 6.5 75.2 109.5 Adelaide Australia 57 3,418.7 3.4 5.5 65.2 94.9 Melbourne Australia 64 3,198.5 3.6 5.0 71.5 104.0 Auckland New Zealand 71 2,655.0 2.0 2.5 50.5 88.1

*Values shown in Australian or New Zealand dollars are indicative and have been converted from the global USD dataset in Turner & Townsend’s Global Construction Market Intelligence 2026 report.

Global ranking of most in demand sectors examined in the report

View the full report here.

Related Articles