Growthpoint Properties Australia (Growthpoint) is pleased to announce its financial results for the six months ended 31 December 2025 (1H26), delivering funds from operations (FFO) of $91.9 million and statutory net profit of $62.6 million, and updating FFO guidance for the 12 months to 30 June 2026 to 23.0 – 23.6 cents per security (cps).

Growthpoint Chief Executive Officer and Managing Director, Ross Lees, said, “I am pleased to announce that we have updated our FY26 FFO guidance to 23.0 to 23.6 cps as we execute our strategy.

“Our dedication to actively managing high-quality assets, and our high-calibre, customer-focused team, has delivered substantial leasing volumes. In our direct portfolio we are on track for record full year office leasing with office occupancy increased to 94% over the half.

“Excellent performance in our industrial portfolio continues to underpin income-driven returns, as existing tenants have taken up new space and we have maintained high occupancy of 98%.

“We are pleased to have created new assets under management, expanding the Growthpoint Australia Logistics Partnership, and launching the Growthpoint Macquarie Park Trust, while delivering liquidity to our syndicate fund investors at the end of investment terms.”

Financial performance

- FFO of $91.9 million, 12.2 cps

- Statutory net profit of $62.6 million, an increase on the statutory net loss of $98.7 million in 1H25, largely resulting from lower net devaluations in investment properties in 1H26

- Distributions per security of 9.2 cps in line with guidance, representing a payout ratio of 75.5% and within the target payout ratio range of 75 – 85% of FFO

- Net tangible assets per security of $3.10, stable relative to $3.09 at 30 June 2025

- Gearing increased to 41.2% from 39.7% as at 30 June 2025, as balance sheet headroom was leveraged to facilitate establishment of new assets under management, and remains in the target range of 35 – 45%

Key operational highlights

- Leasing execution substantially de-risked near-term expiries in the directly held portfolio, and delivered consistent direct portfolio weighted average lease expiry (WALE) of 5.6 years and high occupancy of 95%

- Industrial leasing of 62,566 square metres (sqm) maintained high occupancy at 98% with WALE of 5.7 years

- Office leasing of 30,068 sqm increased occupancy to 94%1 and maintained WALE of 5.5 years

- Terms agreed on a further 30,751 sqm of office leasing at 31 January 20262

- Created $124.9 million of new assets under management (AUM) across the Growthpoint Macquarie Park Trust (GMPT)3 and Growthpoint Australia Logistics Partnership (GALP)

- Delivered liquidity for fund investors, divested $140.0 million AUM, a further $172.8 million settled January

- Achieved Growthpoint’s Net Zero Target on 1 July 20254 and continued to improve NABERS ratings

FY26 guidance

- FY26 FFO guidance updated to 23.0 – 23.6 cps from 22.8 – 23.6 cps following significant leasing in 1H26, distribution guidance of 18.4 cps maintained5

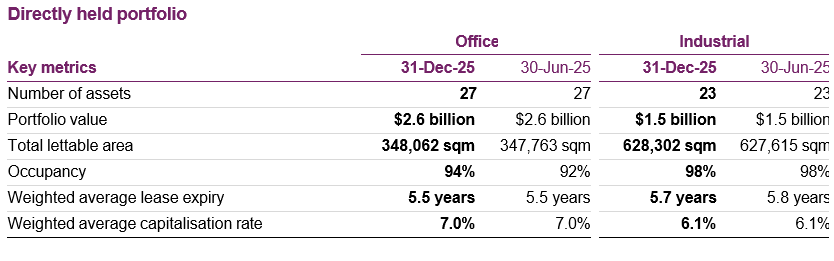

Direct office portfolio

In 1H26, Growthpoint completed 30,068 sqm of leasing in the directly held office portfolio, equivalent to 7.7% of office portfolio income, with an average lease term of 5.6 years, increasing occupancy to 94% from 92% over the half.

Active management including targeted investment resulted in more office leasing being completed in 1H26 than the FY25 full year, and the portfolio is on track for record full year office leasing. FY26 expiries reduced from 11% to 7% over the half, and to 3% proforma for 30,751 sqm with terms agreed as at 31 January 2026.6

Capitalisation rates continued to stabilise in the first half and market rents adopted in direct office portfolio valuations increased by an average of 1.6%, however, the value of the directly held office portfolio declined slightly by $24.0 million or 0.9% on a net basis after accounting for capitalised amounts7 in the half.

Direct industrial portfolio

Over the half year, Growthpoint completed 62,566 sqm of industrial leasing in the directly held portfolio, equivalent to 12.4% of industrial portfolio income, with an average lease term of 4.9 years, maintaining high occupancy of 98%.

Partnering with tenants supported high occupancy and growth for both customers and Growthpoint, with lease renewals with key tenant partners Linfox and Jaguar Land Rover, rapid expansion of the new Panda Mart lease, and existing New South Wales tenant partner IVE Group taking up a site in Western Australia. The directly held industrial portfolio is positioned to deliver income-driven returns as vacancies and forward expiries are now less than 6% per year through to the end of FY29.

Capitalisation rates remained relatively unchanged and market rents adopted in direct industrial portfolio valuations increased by an average of 2.1% and the value of the directly held industrial portfolio increased by 0.2% or $2.5 million on a net basis after accounting for capitalised amounts7 in the half.

In line with the partnership objective, Growthpoint expanded GALP during the half with the acquisition of a $23.6 million industrial asset in Bundamba, Queensland. GALP now holds a total of eight assets, and Growthpoint continues to seek opportunities to further add to the partnership.

Growthpoint established GMPT to acquire a $101.3 million A-Grade office asset in Macquarie Park, the largest metropolitan office market in New South Wales. With a tenancy profile focused on life sciences, medical, and technology businesses, the acquisition offers a deep value, countercyclical opportunity with strong upside potential.

Growthpoint continued to facilitate liquidity for fund investors, realising value and returning capital at the end of investment terms. During the half, $140.0 million of AUM was divested, with a further $172.8 million AUM divestment settled in January 2026.

Sustainability

Growthpoint is proud to have achieved its Net Zero Target9 on 1 July 2025, a significant milestone, and met three out of four performance targets for its Sustainability Linked Loans for the measurement period ending October 2025, achieving a margin discount.

In 1H26, Growthpoint continued to deliver sustainable outcomes, maintaining a GRESB score of 85, above the average score of 79. Our average portfolio NABERS ratings remain strong, with Energy increasing to 5.3 stars at 31 December 2025 (from 5.2 stars at 30 June 2025) and Water rating remaining steady at 4.9 stars. Growthpoint’s average portfolio NABERS Indoor Environment rating increased to 5.2 stars (from 5.0 stars at 30 June 2025) reflecting a continued focus on delivering exceptional tenant environments.

FY26 outlook

Ross Lees said, “We are pleased to update our FFO guidance to 23.0 to 23.6 cps as we have substantially de-risked forward expiries in the first half.

“While the macroeconomic environment remains challenging in the short term, and interest rate uncertainty is ongoing, strong inbound migration along with a tight labour market is expected to underpin long-term demand for office, industrial and retail space.

“Furthermore, supply across all three of these sectors is expected to remain well below historic averages given current constraints driving high economic rents, supporting rental growth and asset values.

“As anticipated, we have seen valuations stabilise across the market and our portfolio.

“Looking forward, we expect to see continued improvement in office markets. While normalising, industrial markets continue to demonstrate sustained demand, generating income-driven returns that underpin the strength of our business.

“Our FY26 priorities are unchanged – following significant de-risking of upcoming expiries across the directly held portfolio, the team is focused on delivering record office leasing by the end of the financial year across current vacancies and upcoming expiries.

“With two transactions completed in the first half, we are continuing to pursue growth through additional funds management opportunities.”

FY26 Guidance

Growthpoint updates FY26 FFO guidance to 23.0 – 23.6 cps from 22.8 – 23.6 cps following significant leasing in 1H26 and maintains distribution guidance of 18.4 cps10. 1H26 FFO is expected to be higher than 2H26 due to the impact of lease and fund expiries affecting 2H26.

A market briefing will be held at 11am (AEDT) today. Click here to register for the webinar or teleconference.

Note: Throughout this document, the asset held by GMPT is included in the third party funds management portfolio for the purpose of portfolio metrics. For financial data purposes, it is consolidated in line with financial reporting.

1 92% as at 30 June 2025.

2 Includes leases signed in January 2026 and under Heads of Agreement (HOA) as at 31 January 2026.

3 GMPT was established in late 2025. Growthpoint’s holding as at 20 February 2026 was 59.0%.

4 Net zero emissions for all scope 1 and scope 2 emissions from our directly managed operationally controlled office assets and some scope 3 emissions from our corporate activities. Growthpoint has proactively purchased and retired carbon credits to offset the majority of our forecast FY26 greenhouse gas emissions that cannot be avoided or reduced. The remaining credits required to fully offset FY26 emissions will be purchased and retired upon finalisation of our FY26 accounts.

5 No acquisitions or disposals of direct investment properties are assumed in providing this guidance. This guidance anticipates no significant market movements or unforeseen circumstances occurring during the remainder of the financial year.

6 Includes leases signed in January 2026 and under Heads of Agreement as at 31 January 2026.

7 Investment property capitalisations including capital expenditure and incentives, net of associated amortisation.

8 Assets under management include $172.8 million relating to Home HQ, with divestment settled in January 2026 for a gross sale price of $180.1 million.

9 Net zero emissions for all scope 1 and scope 2 emissions from our directly managed operationally controlled office assets and some scope 3 emissions from our corporate activities. Growthpoint has proactively purchased and retired carbon credits to offset the majority of our forecast FY26 greenhouse gas emissions that cannot be avoided or reduced. The remaining credits required to fully offset FY26 emissions will be purchased and retired upon finalisation of our FY26 accounts.

10 No acquisitions or disposals of direct investment properties are assumed in providing this guidance. This guidance anticipates no significant market movements or unforeseen circumstances occurring during the remainder of the financial year.

Related Articles